MILPITAS, Calif. – May 16, 2023 – The current global semiconductor manufacturing industry contraction is expected to moderate in the second quarter of 2023 and give way to a gradual recovery starting in the third quarter, SEMI announced in its Q1 2023 publication of the Semiconductor Manufacturing Monitor (SMM) Report, prepared in partnership with TechInsights.

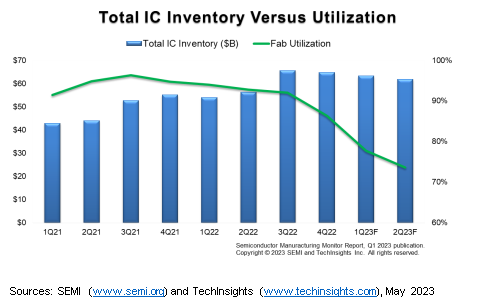

In the second quarter of 2023, industry indicators including IC sales and silicon shipments – both partly supported by seasonality – point to quarter-over-quarter improvements. However, despite the gains, elevated inventories continue to dampen silicon shipments and fab utilization rates remain significantly lower than levels registered last year. In addition, semiconductor equipment sales continue to decline in parallel with capital expenditure adjustments by major industry stakeholders.

The indicators point to a likely bottoming of the current downturn in the second quarter of 2023 with a slow recovery expected to begin in the year’s second half.

“The current market downturn is compounded by soft consumer demand and elevated inventory levels and has led to a sharp decline in semiconductor fab utilization,” said Clark Tseng, Senior Director of Market Intelligence at SEMI. “However, as the inventory correction comes to an end in mid-2023, a mild recovery is expected in the second half of the year driven by a pickup in demand for inventory and the holiday season.”

“Despite ongoing uncertainties and risks, we expect continuing production cuts and capex reductions, especially in the memory market, will start having a positive impact on market fundamentals in the latter part of the year, resulting in a more balanced market environment,” said Risto Puhakka, VP of Market Analysis at TechInsights.

|

The Semiconductor Manufacturing Monitor (SMM) report provides end-to-end data on the worldwide semiconductor manufacturing industry. The report highlights key trends based on industry indicators including capital equipment, fab capacity, and semiconductor and electronics sales, and includes a capital equipment market forecast. The SMM report also contains two years of quarterly data and a one-quarter outlook for the semiconductor manufacturing supply chain including leading IDM, fabless, foundry, and OSAT companies. An SMM subscription includes quarterly reports.

Download an SMM report sample.

For more information or to subscribe, please contact the SEMI Market Intelligence Team at mktstats@semi.org. More information is also available at SEMI Market Data.

About SEMI

SEMI® connects more than 2,500 member companies and 1.3 million professionals worldwide to advance the technology and business of electronics design and manufacturing. SEMI members are responsible for the innovations in materials, design, equipment, software, devices, and services that enable smarter, faster, more powerful, and more affordable electronic products. Electronic System Design Alliance (ESD Alliance), FlexTech, the Fab Owners Alliance (FOA), the MEMS & Sensors Industry Group (MSIG), Nano-Bio Materials Consortium (NBMC), and SOI Consortium are SEMI Strategic Technology Communities. Visit

www.semi.org, contact one of our worldwide offices, and connect with SEMI on

LinkedIn and

Twitter to learn more.

Association Contact

Michael Hall/SEMI

Phone: 1.408.943.7988

Email:

mhall@semi.org

Animation, 3D Art and 3D Models")