- Record home equity and government protections keep foreclosure rates at historic lows

- Overall delinquency rates have declined from a peak in May but remain nearly double 2019’s rates

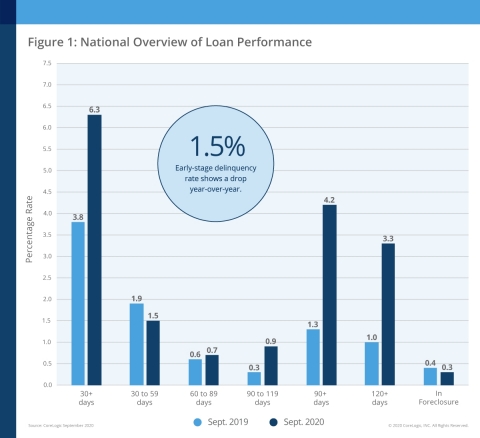

IRVINE, Calif. — (BUSINESS WIRE) — December 8, 2020 — CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report for September 2020. On a national level, 6.3% of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure). This represents a 2.5-percentage point increase in the overall delinquency rate compared to September 2019, when it was 3.8%.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20201208005292/en/

CoreLogic National Overview of Mortgage Loan Performance, featuring September 2020 Data (Graphic: Business Wire)

To gain an accurate view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency, including the share that transitions from current to 30 days past due. In September 2020, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.5%, down from 1.9% in September 2019, and down from 4.2% in April when early-stage delinquencies spiked.

- Adverse Delinquency (60 to 89 days past due): 0.7%, up from 0.6% in September 2019, but down from 2.8% in May, when adverse-stage delinquencies peaked.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 4.2%, up from 1.3% in September 2019, but down slightly from 4.3% in August.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, down from 0.4% in September 2019. The September 2020 foreclosure rate has stayed at 0.3% for six consecutive months, which was the lowest since at least January 1999.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.8%, unchanged from September 2019. The transition rate has slowed since April 2020, when it peaked at 3.4%.

Borrowers who fell behind on their mortgages early this year continue to move through the delinquency funnel. Still, foreclosures remain low and in September, serious delinquencies leveled out for the first time since April. This is in part due to the Dodd-Frank Act, which limits consumer exposure to risky-lending practices; the CARES Act, which affords borrowers more time to seek financial stability; and a record amount of home equity fueled by rapid home price growth, which provides a buffer against foreclosure.

“Although delinquencies remain high, it’s clear the economy has passed an initial stress test. High home equity balances and structural protections put in place as a result of the Great Recession contributed to surviving this test," said Frank Martell, president and CEO of CoreLogic. "Housing demand remains strong, and rates low, which provides optimism that the housing market will continue to be a bright spot in this COVID-ravaged economy.”

“Our analysis of CoreLogic public records shows that more than one-half of all home mortgage loans created since the onset of the pandemic have been no-cash-out refinance,” said Dr. Frank Nothaft, chief economist at CoreLogic. “By reducing their mortgage rate with these types of loans, homeowners have been lowering both their interest expense and risk of delinquency.”

In September, every state logged an annual increase in overall delinquency rates. For months, popular tourism destinations showed the highest increases, with Nevada (up 4.9 percentage points), Hawaii (up 4.7 percentage points) and Florida (up 4 percentage points) again topping the list for gains in September.

Similarly, nearly all U.S. metro areas logged an increase in overall delinquency rates in September. Lake Charles, Louisiana — where Hurricane Laura hit in August — experienced the largest annual increase of 10.7 percentage points. Other metro areas with significant overall delinquency increases included Odessa, Texas (up 10.3 percentage points), Midland, Texas (up 7.9 percentage points) and Kahului, Hawaii (up 7.5 percentage points).

The next CoreLogic Loan Performance Insights Report will be released on January 12, 2020, featuring data for October 2020. For ongoing housing trends and data, visit the CoreLogic Insights Blog: www.corelogic.com/insights.

Methodology

The data in The CoreLogic LPI report represents foreclosure and delinquency activity reported through September 2020. The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure and are, therefore, excluded from the analysis. CoreLogic has approximately 75% coverage of U.S. foreclosure data.

Source: CoreLogic

The data provided is for use only by the primary recipient or the primary recipient's publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient's parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Valerie Sheets at newsmedia@corelogic.com. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic (NYSE: CLGX), the leading provider of property insights and solutions, promotes a healthy housing market and thriving communities. Through its enhanced property data solutions, services and technologies, CoreLogic enables real estate professionals, financial institutions, insurance carriers, government agencies and other housing market participants to help millions of people find, buy and protect their homes. For more information, please visit www.corelogic.com.

CORELOGIC and the CoreLogic logo are trademarks of CoreLogic, Inc. and/or its subsidiaries. All other trademarks are the property of their respective owners.

View source version on businesswire.com: https://www.businesswire.com/news/home/20201208005292/en/

Contact:

Valerie Sheets

CoreLogic

newsmedia@corelogic.com

Animation, 3D Art and 3D Models")