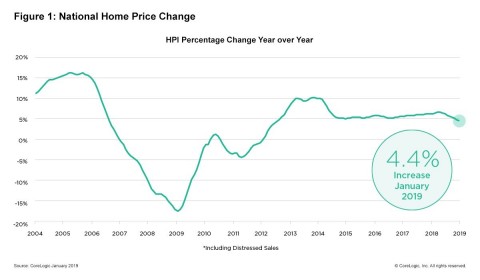

- Twelve-month home-price growth rate was slowest since August 2012

- HPI Forecast indicates annual average home price to increase 3.4 percent from 2018 to 2019

- Since peaking at 6.6 percent last April, annual home price gains have declined or held steady each month

IRVINE, Calif. — (BUSINESS WIRE) — March 5, 2019 — CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released the CoreLogic Home Price Index (HPI™) and HPI Forecast™ for January 2019, which shows home prices rose both year over year and month over month. Home prices increased nationally by 4.4 percent year over year from January 2018. On a month-over-month basis, prices increased by 0.1 percent in January 2019. ( December 2018 data was revised. Revisions with public records data are standard, and to ensure accuracy, CoreLogic incorporates the newly released public data to provide updated results each month.)

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190305005121/en/

CoreLogic National Home Price Change; January 2019. (Graphic: Business Wire)

Looking ahead, the CoreLogic HPI Forecast indicates that the 2019 annual average home price will increase 3.4 percent above the 2018 annual average. On a month-over-month basis, home prices are expected to decrease by 0.9 percent from January 2019 to February 2019. The CoreLogic HPI Forecast is a projection of home prices calculated using the CoreLogic HPI and other economic variables. Values are derived from state-level forecasts by weighting indices according to the number of owner-occupied households for each state.

“The spike in mortgage interest rates last fall chilled buyer activity and led to a slowdown in home sales and price growth,” said Dr. Frank Nothaft, chief economist for CoreLogic. “Fixed-rate mortgage rates have dropped 0.6 percentage points since November 2018 and today are lower than they were a year ago. With interest rates at this level, we expect a solid home-buying season this spring.”

According to the CoreLogic Market Condition Indicators (MCI), an analysis of housing values in the country’s 100 largest metropolitan areas based on housing stock, 35 percent of metropolitan areas have an overvalued housing market as of January 2019. The MCI analysis categorizes home prices in individual markets as undervalued, at value or overvalued, by comparing home prices to their long-run, sustainable levels, which are supported by local market fundamentals (such as disposable income). Additionally, as of January 2019, 27 percent of the top 100 metropolitan areas were undervalued, and 38 percent were at value.

When looking at only the top 50 markets based on housing stock, 40 percent were overvalued, 18 percent were undervalued and 42 percent were at value in January 2019. The MCI analysis defines an overvalued housing market as one in which home prices are at least 10 percent above the long-term, sustainable level. An undervalued housing market is one in which home prices are at least 10 percent below the sustainable level.

“The slowing growth in home prices was inevitable in many respects as buyers pull back in the face of higher borrowing and ownership costs,” said Frank Martell, president and CEO of CoreLogic. “As we head into 2019, we can expect continued strong employment growth and rising incomes which could support a reacceleration in home-price appreciation later this year.”

The next CoreLogic HPI press release, featuring February 2019 data, will be issued on Tuesday, April 2, 2019 at 8:00 a.m. ET.

Methodology

The CoreLogic HPI™ is built on industry-leading public record, servicing and securities real-estate databases and incorporates more than 40 years of repeat-sales transactions for analyzing home price trends. Generally released on the first Tuesday of each month with an average five-week lag, the CoreLogic HPI is designed to provide an early indication of home price trends by market segment and for the “Single-Family Combined” tier, representing the most comprehensive set of properties, including all sales for single-family attached and single-family detached properties. The indices are fully revised with each release and employ techniques to signal turning points sooner. The CoreLogic HPI provides measures for multiple market segments, referred to as tiers, based on property type, price, time between sales, loan type (conforming vs. non-conforming) and distressed sales. Broad national coverage is available from the national level down to ZIP Code, including non-disclosure states.

CoreLogic HPI Forecasts™ are

based on a two-stage, error-correction econometric model that combines

the equilibrium home price—as a function of real disposable income per

capita—with short-run fluctuations caused by market momentum,

mean-reversion, and exogenous economic shocks like changes in the

unemployment rate. With a 30-year forecast horizon, CoreLogic HPI

Forecasts project CoreLogic HPI levels for two tiers — “Single-Family

Combined” (both attached and detached) and “Single-Family Combined

Excluding Distressed Sales.” As a companion to the CoreLogic HPI

Forecasts, Stress-Testing Scenarios align with Comprehensive Capital

Analysis and Review (CCAR) national scenarios to project five years of

home prices under baseline, adverse and severely adverse scenarios at

state, Core Based Statistical Area (CBSA) and ZIP Code levels. The

forecast accuracy represents a 95-percent statistical confidence

interval with a +/- 2 percent margin of error for the index.

Animation, 3D Art and 3D Models")