- U.S. serious delinquency rate was the lowest since November 2006

- Total past due and serious delinquency rates were down annually in October in all states except North Dakota, where the rates remained unchanged

- Some hurricane-affected metros in the Carolinas and Florida Panhandle suffer jumps in key delinquency rates

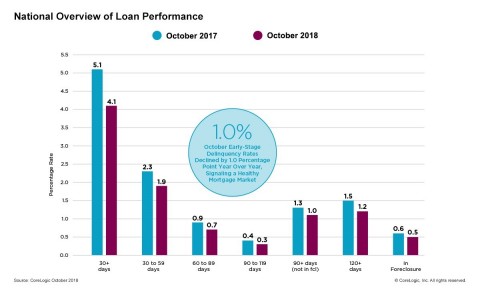

IRVINE, Calif. — (BUSINESS WIRE) — January 8, 2019 — CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report. The report shows that, nationally, 4.1 percent of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure) in October 2018, representing a 1 percentage point decline in the overall delinquency rate compared with October 2017, when it was 5.1 percent. This was the lowest for the month of October in at least 18 years.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190108005146/en/

CoreLogic National Overview of Mortgage Loan Performance, featuring October 2018 Data. (Graphic: Business Wire)

As of October 2018, the foreclosure inventory rate – which measures the share of mortgages in some stage of the foreclosure process – was 0.5 percent, down 0.1 percentage point since October 2017. The October 2018 foreclosure inventory rate tied with the April, May, June, July, August and September rates this year as the lowest for any month since September 2006 and also marked the lowest rate for an October since 2005. In both instances, the foreclosure inventory rate was 0.5 percent.

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To monitor mortgage performance comprehensively, CoreLogic examines all stages of delinquency, as well as transition rates, which indicate the percentage of mortgages moving from one stage of delinquency to the next.

The rate for early-stage delinquencies – defined as 30 to 59 days past due – was 1.9 percent in October 2018, down from 2.3 percent in October 2017. The share of mortgages that were 60 to 89 days past due in October 2018 was 0.7 percent, down from 0.9 percent in October 2017. The serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – was 1.5 percent in October 2018, down from 1.9 percent in October 2017. This serious delinquency rate was the lowest for an October since 2006 when it was 1.5 percent. It ties August and September 2018 as the lowest for any month since March 2007 when it was also 1.5 percent.

Since early-stage delinquencies can be volatile, CoreLogic also analyzes transition rates. The share of mortgages that transitioned from current to 30 days past due was 0.8 percent in October 2018, down from 1.1 percent in October 2017. By comparison, in January 2007, just before the start of the financial crisis, the current-to-30-day transition rate was 1.2 percent, while it peaked in November 2008 at 2 percent.

“While the strong economy has helped families stay current and push overall delinquency rates lower, areas that were hit hard by natural disasters have seen a rise in loan defaults,” said Dr. Frank Nothaft, chief economist for CoreLogic. “The 30-day delinquency rate in the Panama City, Florida metro area tripled between September and October 2018 as a result of Hurricane Michael. Two months after Hurricane Florence made landfall in the Carolinas, 60-day delinquency rates doubled in the Jacksonville, Wilmington, New Bern and Myrtle Beach metro areas. And buffeted by Kilauea’s eruption in the Hawaiian Islands, serious delinquency rates jumped on the Big Island by 9 percent between June and October 2018, while falling by 4 percent in the rest of Hawaii.”

Hurricane Irma and Hurricane Florence (2017 and 2018, respectively) continue to impact some metropolitan areas, with mortgages transitioning from current to 30 days past due. This October, 18 metropolitan areas posted an annual increase in overall delinquency rate, seven of which were either in North or South Carolina. In the coming months, CoreLogic will continue to monitor these and other metros struck by natural disaster for potential increase in delinquencies.

“Despite some regional spikes related to hurricane and fire impacted areas, overall delinquency rates are near or at historic lows,” said Frank Martell, president and CEO of CoreLogic.

For ongoing housing trends and data, visit the CoreLogic Insights Blog: www.corelogic.com/insights.

Methodology

The data in this report represents foreclosure and delinquency activity reported through October 2018.

The data in this report accounts for only first liens against a property

and does not include secondary liens. The delinquency, transition and

foreclosure rates are measured only against homes that have an

outstanding mortgage. Homes without mortgage liens are not typically

subject to foreclosure and are, therefore, excluded from the analysis.

Approximately one-third of homes nationally are owned outright and do

not have a mortgage. CoreLogic has approximately 85 percent coverage of

U.S. foreclosure data.

Animation, 3D Art and 3D Models")