- Early-Stage Delinquencies Drop 0.1 Percentage Points Year Over Year in May

- Florida was the Only State to Post an Annual Increase in Overall Delinquency Rate

- Existing Mortgages at Risk in Regions Impacted By Current Wildfires

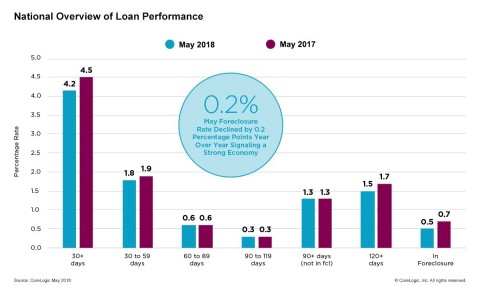

IRVINE, Calif. — (BUSINESS WIRE) — August 14, 2018 — CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report. The report shows that, nationally, 4.2 percent of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure) in May 2018, representing a 0.3 percentage point decline in the overall delinquency rate compared with May 2017, when it was 4.5 percent.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20180814005204/en/

CoreLogic National Overview of Mortgage Loan Performance, featuring May 2018 Data (Graphic: Business Wire)

As of May 2018, the foreclosure inventory rate – which measures the share of mortgages in some stage of the foreclosure process – was 0.5 percent, down 0.2 percentage points from 0.7 percent in May 2017. The May 2018 foreclosure inventory rate was the lowest for any month since September 2006, when it was also 0.5 percent, and it was the lowest for May since 2006.

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To monitor mortgage performance comprehensively, CoreLogic examines all stages of delinquency, as well as transition rates, which indicate the percentage of mortgages moving from one stage of delinquency to the next.

The rate for early-stage delinquencies – defined as 30 to 59 days past due – was 1.8 percent in May 2018, down from 1.9 in May 2017. The share of mortgages that were 60 to 89 days past due in May 2018 was 0.6 percent, unchanged from May 2017. The serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – was 1.8 percent in May 2018, down from 2 percent in May 2017. The May 2018 serious delinquency rate was the lowest for that month since 2007, when it was 1.6 percent.

Since early-stage delinquencies can be volatile, CoreLogic also analyzes transition rates. The share of mortgages that transitioned from current to 30 days past due was 0.8 percent in May 2018, unchanged from 0.8 percent in May 2017. By comparison, in January 2007, just before the start of the financial crisis, the current- to 30-day transition rate was 1.2 percent, while it peaked in November 2008 at 2 percent.

“While the strong economy has nudged serious delinquency rates to their lowest level in 12 years, areas hit by natural disasters have had increases,” said Dr. Frank Nothaft, chief economist for CoreLogic. “The tragic wildfires in the West will likely lead to a spike in delinquencies in hard-hit neighborhoods. As an example, the wildfire in Santa Rosa last year destroyed or severely damaged more than 5,000 homes. Delinquency rates rose in the aftermath, and in the ensuing months we observed home-price growth accelerate and sales decline. We will likely see the same scenario unfold in fire-ravaged communities this year.”

In California, where current delinquency rates are well below the national level, the regions impacted by recent wildfires are becoming more susceptible to mortgages entering some stage of delinquency as the fires continue to burn. According to a recent Carr Fire analysis by CoreLogic, the 2018 season is outpacing 2017 with more than 292,000 acres burned this year thus far. The Carr Fire outside the city of Redding and the French Gulch community presented the greatest risk to homeowners with CoreLogic estimating a total of $3.5 billion potential reconstruction costs in that area.

“Serious delinquency rates continue to remain lower than a year earlier except in Florida and Texas, the hardest-hit states during last year’s hurricane season,” said Frank Martell, president and CEO of CoreLogic. “We have observed continued challenges for families to make mortgage payments in regions impacted during the 2017 Hurricane season. For the coming months, we will monitor mortgage and housing trends in areas now plagued by wildfires, particularly in California, Montana, and Arizona.”

For ongoing housing trends and data, visit the CoreLogic Insights Blog: www.corelogic.com/insights.

Methodology

The data in this report represents foreclosure and delinquency activity reported through May 2018.

The data in this report accounts for only first liens against a property

and does not include secondary liens. The delinquency, transition and

foreclosure rates are measured only against homes that have an

outstanding mortgage. Homes without mortgage liens are not typically

subject to foreclosure and are, therefore, excluded from the analysis.

Approximately one-third of homes nationally are owned outright and do

not have a mortgage. CoreLogic has approximately 85 percent coverage of

U.S. foreclosure data.

Animation, 3D Art and 3D Models")